Monolithic investor Warren Buffet said, “Risk comes from not knowing what you’re doing.” As a business owner, you keep a pulse on every facet of your company. But no matter how well you manage your operations, each business decision you make carries risk. If you don’t know what you’re doing to mitigate that risk or prepare to respond, your company could suffer. How can you get a better handle on your business’s risk profile and proactively control risk? We’ve got you covered.

In this guide, we’ll discuss:

- What is risk management and why is it important?

- What are the types of risk?

- 4 foundational steps for your risk management plan

- Insurance as a risk mitigation technique

- The power of a comprehensive risk management partner

What is risk management and why is it important?

Risk management is identifying, assessing, and prioritizing risks that can impact a business, and then mitigating or planning for those risks. It’s important because it helps reduce uncertainty, and allows business owners to make informed decisions to protect themselves against potential losses.

What is the goal of risk mitigation?

Risk mitigation aims to reduce the likelihood and impact of risk. Businesses mitigate risk by using measures that prevent, minimize, or transfer risks, based on their potential severity and the resources available to address them.

Why do we mitigate risk? While it’s impossible to avoid every risk, strategic planning can help reduce the likelihood of an undesirable event, and minimize its impact on the business if it does occur.

What are the types of risk?

Your business could face a wide range of potential risks, but there are four main types of risk:

Most companies face some level of all these types of risk. Let’s dig into what each entails and some examples.

Operational Risk

Operational risk is the risk of loss resulting from your day-to-day operations. It includes the inadequacy or failure of internal processes, people, and systems. It can also include risk from external events. Here are some examples of operational risk:

- Technology failures

- Employee errors

- Supply chain disruptions

- Business process failures

- Fraud

- Natural disasters

Financial risk

Financial risk is the risk of losing money from an investment or business decision. It encompasses fluctuations in market conditions, credit risk, and liquidity risk.

Some examples of financial risk are:

- Interest rate fluctuation

- Exchange rate volatility

- Credit defaults

- Market crashes

- Depreciation of asset values

- Theft or damage to owned assets

Legal and compliance risk

Compliance risk is the risk of legal repercussions and financial loss due to a company’s failure to comply with the laws and regulations. The consequences could include regulatory penalties and fines

Here are some examples of legal and compliance risk:

- Noncompliance with regulations

- Data privacy breaches or violations

- OSHA compliance

Strategic risk

Strategic risks are events or decisions that could threaten your company’s ability to achieve its goals and deliver expected outcomes.

Examples of strategic risk include:

- Entering a new market

- Over-reliance on a single supplier

- Changes in senior leadership

- Mergers and acquisitions

- Industry or market changes

- Reputational risk

What’s in a risk mitigation plan? 4 foundational steps

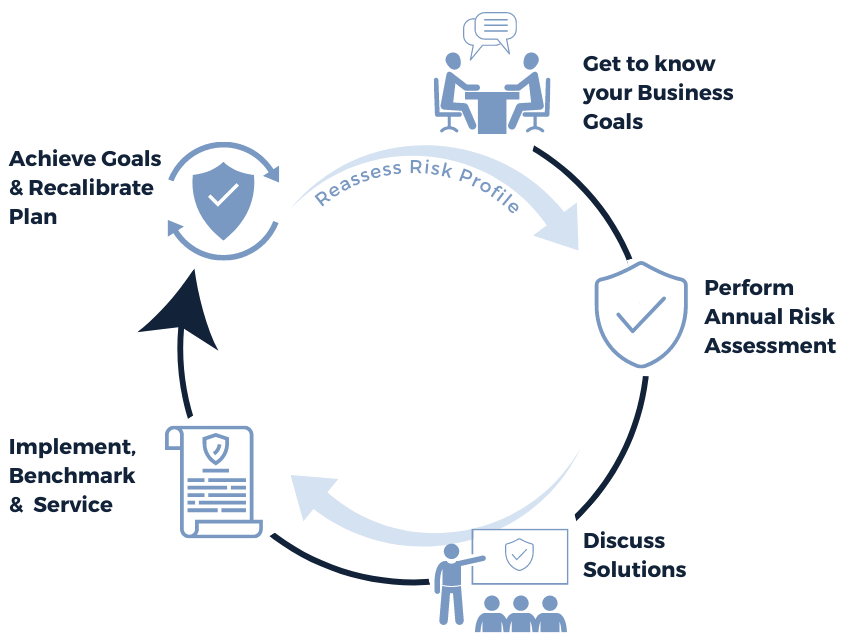

Your risk mitigation strategy should be as unique as your business. At POWERS, we take every client through a consultative risk management process to build a plan tailored to their industry and business goals.

These are the four foundational steps we use.

1. Identify and assess risks

Now that you’re familiar with the most common types of risks, your first step is to figure out which of them apply to your company.

The best method for thorough and efficient risk identification is to get all stakeholders in a room together and brainstorm. Getting a variety of perspectives will help you perform a well-rounded risk assessment.

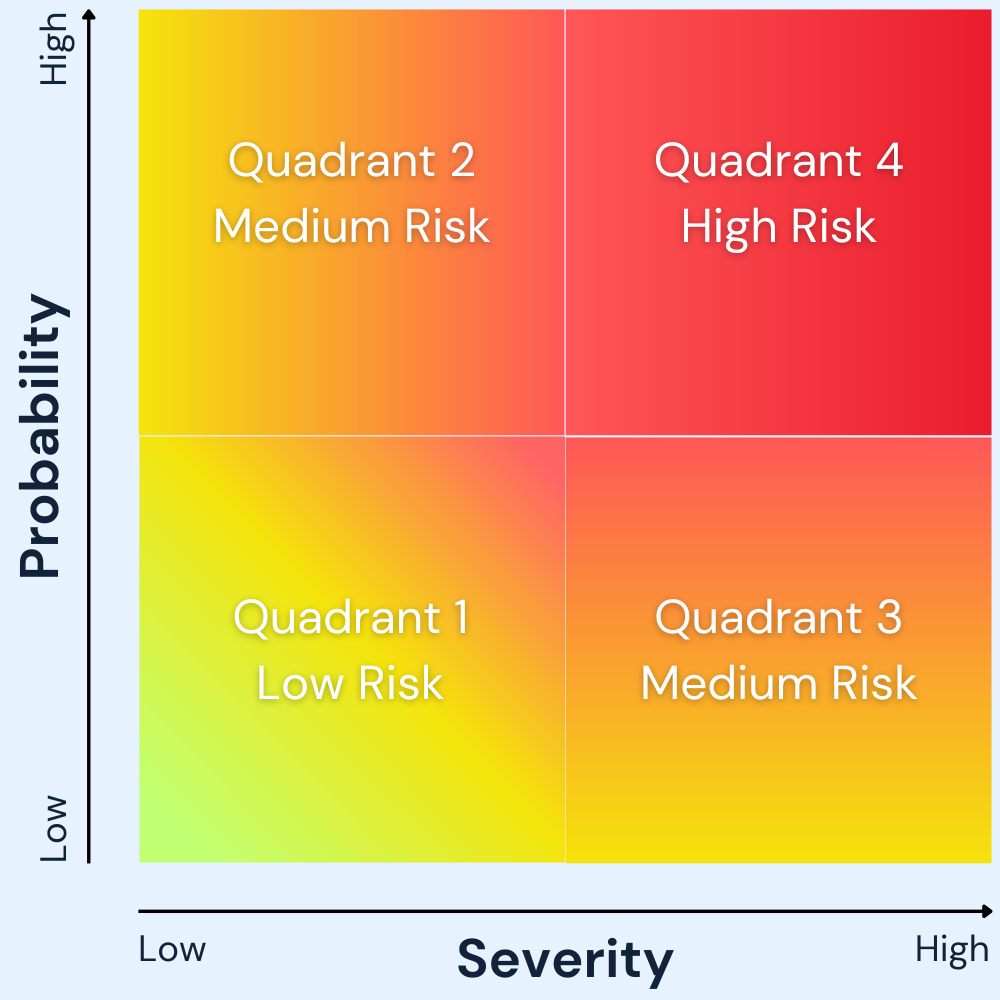

If you identified a large number of potential risks, don’t panic. All risks are not created equal. Your goal is to devote the most resources to controlling the most important risks.

There are two factors that determine a risk’s importance: probability and severity. Look at the list of risks you identified and answer two questions for each of them:

- Probability: What is the likelihood that this risk will happen?

- Severity: What are the potential costs if it does?

A risk assessment framework will help you prioritize the risks and decide how you will respond to them. This kind of quantitative risk analysis can also be visualized using a quadrant.

An outside perspective can be very valuable for this step. We do a full exposure analysis with all our POWERS clients to uncover and assess your exposures, both common and uncommon.

2. Decide how to approach each risk

Once you’ve prioritized your top risks, designate one “risk owner” for each. This is a simple but crucial step to make sure the appropriate action is taken.

The risk owner should be someone who:

- Works in the area impacted by the risk

- Has the authority to address the risk

Of course, the risk owner can team up with others in the company to tackle the risk, but they’re the one accountable for it at the end of the day.

The risk owners now have the responsibility of leading the company’s approach to each risk. You have four options:

- Avoid the risk altogether. Sometimes, the best decision is to avoid a risk with high probability and severity. Risk avoidance might seem like a no-brainer, but it’s often unrealistic for most risks.

- Transfer the risk to another party. Any work that involves contracts is an opportunity for risk transfer. For example, you can require a subrogation waiver on a subcontractor’s insurance policy. Insurance itself is also a form of risk transference.

- Mitigate and minimize the risk as best you can. This is likely the approach your company will take with most risks. Risk mitigation inherently involves trade-offs. Your job is to compare the cost of control measures to the probability and severity of the risk.

- Accept the risk and its implications. No business is risk-free. Some risks are simply a cost of doing business. For risks that are low probability and low severity, risk acceptance is a reasonable approach. The resources to mitigate, transfer, or avoid the risk are just not worth it.

The way you approach a risk can make a big difference in its potential impact on your business. A solid risk management plan can prevent incidents from happening in your workplace. It also helps you foster goodwill with your insurance carrier by showing that you’re proactive about controlling risk.

This is where having a specialized partner really adds value to your risk mitigation planning. For example, all POWERS clients benefit from these consultative services to mitigate risk:

| In-house claims consultant | We’ll help you protect and control your claims costs, and advocate for you throughout the claims process. |

| Safety program, education, and training | Keep safety top of mind to prevent claims, protect your employees, and protect your business from litigation. |

| Audit assistance | Prepare for your workers’ comp audit to ensure you’re not overcharged, and you only pay for your exposures. |

| Loss retention and control analysis | Understand your exposures and develop plans to reduce the frequency and severity of losses. |

| Exposure analysis | Discover your unknown exposures to protect your business from an adverse financial event. |

| Work comp e-mod forecasting | Understand how different factors will impact your e-mod and eligibility to bid on jobs. |

| OSHA compliance and reporting | Stay compliant with the latest OSHA regulations to avoid costly penalties. |

| Contract alignment review | Get expert feedback on your contractual obligations to make sure your third-party exposures are covered. |

| Balance sheet analysis | Increase your bonding capacity with an in-depth look at your debt, equity, and liquidity. |

3. Plan to respond to risk events

One of the most important parts of the risk management process is being prepared to act if a risk event does occur. Unless you’ve chosen to completely avoid a risk, there’s a chance it could happen. For example, no one can prevent natural disasters – the best we can do is be prepared.

Your risk response plan could be as simple as “file an insurance claim.” But the higher priority the risk, the more detailed your response plan should be. If an event has the potential to disrupt business operations in a huge way, you need thorough business continuity and disaster recovery plans.

It’s crucial to document these plans ahead of time and use them to train the relevant employees. Because when minutes matter, you won’t have time to deliberate a response.

4. Monitor risks

The risks you face tomorrow might not be the same as those you face today. Doing a risk assessment once and letting the report collect dust will not help you protect your business in any tangible way.

It’s vital to monitor your company’s risk profile as it evolves and make sure your responses are still appropriate. Repeat the steps of this risk management plan regularly and keep a pulse on external risk factors.

If you don’t have a dedicated risk manager internally (or even if you do), this can be a tall order. But without an intentional and consistent process, you could face the unexpected consequences of a risk event. Working with a third-party risk management partner can help you identify and respond to new risks.

Insurance as a risk mitigation tool

Where does insurance fit into your risk management plan? You can’t eliminate every risk your business faces. Insurance is a tool that lets you transfer the financial risk of certain types of losses to your carrier.

As you consider risk management strategies, you can assess which types of insurance policies might make sense for your business given the risks you face. For example, liability policies can help you hedge against legal risk. Property insurance can protect against operational risk. It’s all about your unique risk profile.

The power of a comprehensive risk management partner

Doing a complete risk assessment to get to the heart of your business’s most crucial risk goals is challenging but important.

Luckily, it’s something we do every day with POWERS clients. We’ve developed a proprietary, systematic approach to all the steps we’ve discussed. The result? A full risk management plan tailored to your business.

And once the plan’s in place, we’ll help you execute it too. As your risk partner, we have experts dedicated to supporting you in every area, from providing employee safety training to managing insurance claims.

We call it consultative risk management. You’ll call it an essential business partnership.