As a business owner, you’ve probably heard the term “experience modification factor” – or “e-mod” – when discussing your workers’ compensation insurance.

You might know that this factor looks at your previous claims to adjust your workers’ comp premium higher or lower.

But what exactly goes into your e-mod and how can you keep work comp costs low if you have a claim? Here’s an overview.

What is an experience modification factor?

Simply put, your business’s experience modification rate is a number that adjusts your workers’ compensation premium up or down based on your company’s claims history.

It’s a small number with a big influence.

An e-mod of 1.0 reflects your industry’s average loss experience. If your mod is higher than 1.0, you’ve had worse claims than is typical of your peers. Your workers’ compensation premium will be higher

If your mod is below 1.0, your claims have been better than the industry average. You’re predicted to be less costly to your workers’ comp carrier, so your premium will be lower.

Importance of understanding your e-mod

Your e-mod has a big impact on your workers’ compensation insurance costs and, therefore, your business’s cash flow. A high e-mod could mean you’re paying 25% or 50% more premium than your competitor with a lower mod. That puts a dent in your bottom line and hampers your ability to compete.

On the other hand, even a small improvement in your e-mod can keep more cash in your pocket by reducing one of your biggest expenses. Improving your mod from 1.0 to 0.9 can help larger businesses save thousands of dollars annually.

Chris Sullivan, Commercial Lines Practice Leader at POWERS, explains just how vital it is to understand your experience rating:

Workers’ comp is often one of a business’s largest line items. And out of all the insurance policies a business owner purchases, it’s the one they have the most control over. With a successful safety program and claims management processes, businesses can significantly impact their workers’ comp costs.

- Chris Sullivan, CLCS, PWCA, Commercial Lines Practice Leader

In some industries, like construction, your e-mod affects more than your insurance premium costs. Larger jobs often include an e-mod bid qualifier – meaning your e-mod has to be less than a specific number to even bid on the job.

Understanding the factors that influence your e-mod helps you proactively control workers’ compensation costs. With the right practices, you can work to minimize your company’s risks and keep your mod low, even in the face of claims.

Factors that impact your e-mod

Your e-mod is about more than just your number of workers’ comp claims or how much they cost. Let’s take a look at three important factors:

- Actual losses and expected losses

- Claims management practices

- Experience period

Actual losses vs. expected losses

When it comes to the experience modification calculation, your claims history doesn’t exist in a bubble. Your mod hinges on a comparison between the claims your company actually incurred and the claims that would be expected for a business of your size and type.

In most states, e-mods are calculated by the National Council on Compensation Insurance. This independent council seeks to predict your expected losses using data across your industry. If your actual losses are higher than expected, your e-mod will rise. If they’re lower than expected, your e-mod will fall.

For example, a hospital and an accounting firm may both have e-mods of 1.1. However, since they’re both compared to their respective industries, the hospital will still be expected to have significantly higher claim frequency and severity than the accounting firm.

Claims management practices

The workers’ comp losses you incur for your carrier depend on two factors: frequency (the number of claims you have) and severity (the total cost of those claims).

After all, a desk worker with a sprained ankle may be able to come to work the next day and fully recover with rest alone. There’s a big difference between that claim and a lineman who was electrocuted and may never recover full use of his arm.

According to Sullivan, what matters most is properly navigating the claims process.

What we explain to our clients is that if your business has a workers’ compensation claim, it doesn’t automatically mean your e-mod is destroyed. There’s a lot you can do to minimize the claim’s impact on your mod.

- Chris Sullivan, CLCS, PWCA, Commercial Lines Practice Leader

A successful claims management plan includes:

- Prompt injury reporting to get the injured employee the medical care they need quickly

- Directing medical care when possible, and collaborating with healthcare providers

- Creating a return-to-work plan with the employee and care providers

- Bringing the employee back to work quickly and safely by offering light duty options

These strategies help you reduce overall claim costs, which minimizes the impact of claims on your e-mod.

E-mod experience period and valuation date

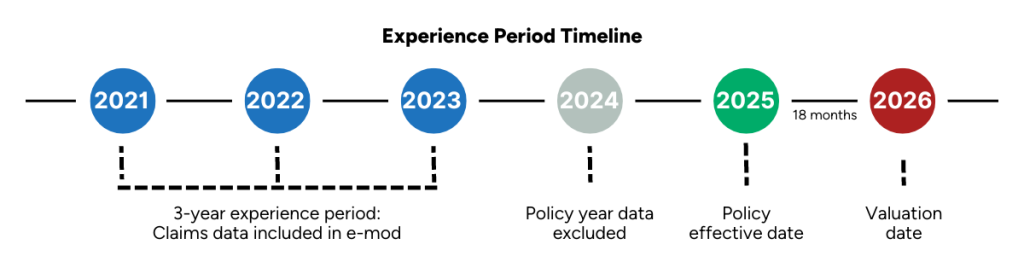

E-mods are calculated annually, but the information incorporated includes policy periods dating back almost four years. The window of time that your workers’ comp claims data is evaluated is known as the “experience period.”

The experience period typically includes the three years prior to the previous year. For example, if your workers’ compensation policy effective date is in 2025, claims data from 2024 is likely not finalized – and therefore is not included in your experience period. Your e-mod calculation would include claims data from 2021, 2022, and 2023.

The valuation date is the date policy data is locked in for your e-mod calculation. It is 18 months from your policy effective date. For example, if your effective date is in June 2025, your valuation date will be in December 2026. That means in the future, your 2027 e-mod will be based on data reported by December 2026, which will affect your 2028 e-mod calculation. If claims activity changes after the valuation date, an adjustment will be made in December 2027.

The moral of the story is that workers’ compensation claims can span long periods of time – and impact your e-mod for a long time. That’s why it’s so important to prevent claims with a safety program and have processes in place to manage claim costs from the beginning.

Your business, your experience, your e-mod

Understanding the factors that go into your workers’ compensation e-mod is critical to controlling one of your biggest insurance expenses. Business owners can minimize workplace injuries and their associated costs with programs like:

- Workplace safety program

- Claims management program

- Return-to-work program

If your e-mod is above 1.0, it’s not the end of the world. Consider it a wake-up call – and an opportunity. With the right practices, you can course correct and bring your rating back down over time.

At POWERS, workers’ compensation is one of our specialties. Our experts can forecast your e-mod and help you create strategies to improve it. To get started, get in touch today.