Iconic American actress Lily Tomlin said, “The road to success is always under construction.”

We can say with certainty that a road to somewhere is always under construction. Who’s building them?

Road contractors.

Highway and road construction companies build and maintain the infrastructure that helps us get safely from point A to point B.

However, every construction project comes with potential risks and liabilities. With the right insurance coverage, you can protect your business, employees, and clients from incidents.

In this guide, we’ll cover:

- Why do road construction companies need insurance?

- What types of insurance do highway and road construction businesses need?

- How much does road construction insurance cost?

- Growing your road construction business with surety bonds

- Managing risk in highway and road construction

- Choosing a risk partner that understands your road construction business

Why do road construction companies need insurance?

Highway and road construction companies need insurance because their work involves significant financial, legal, and reputational risks. The right insurance coverage protects your firm from costly accidents, project delays, and professional errors.

For example, construction is one of the most hazardous industries to work in. Road contractors often do their work near busy roadways. The presence of fast-moving vehicles with distracted drivers is a serious safety hazard. Insurance can help cover medical bills and lost wages resulting from workplace injuries.

Here’s another one: Road projects have complex timelines with many subcontractors and dependencies. Delays caused by weather events or supply chain disruptions can put the whole project at risk.

What types of insurance do highway and road construction businesses need?

Road construction companies have a lot on the line. Insurance is a critical part of managing the risk associated with large projects, workers with specialized skills, and physically-demanding work environments.

There are many factors that influence your insurance strategy. That’s why we take a consultative approach at POWERS. We need a thorough understanding of your operations, exposures, and goals to recommend the best insurance solutions for you.

Once we’ve done your risk assessment, here are some of the policies we might recommend.

General liability

General liability insurance covers claims that your business caused third-party injury or property damage. It helps protect your company from financial losses due to lawsuits or other legal claims stemming from your operations such as a trip and fall, illness, or even personal injury.

When we recommend a general liability policy

Your state or commercial contracts might require you to carry general liability coverage. Even if not required, GL provides fundamental protection for your business. We recommend it for every business that interacts with the public or customers.

Commercial property

Commercial property insurance protects your building and physical property from events like:

- Fire

- Theft

- Vandalism

- Hail, windstorms, lightning

- Natural disasters

It covers financial losses from property damage, lost income, and other expenses while recovering.

When we recommend commercial property

We recommend commercial property coverage for most businesses that own or rent property, including buildings, equipment, inventory, and supplies.

Workers’ compensation

In most states, businesses with a certain number of employees must carry workers’ compensation. Workers’ comp covers medical bills and lost wages for employees who are injured or become ill on the job.

When we recommend workers’ comp

This no-fault insurance policy protects you and your employees from the financial impact of workplace injuries. Each state has different workers’ comp requirements, but we recommend it for most businesses with employees.

Inland marine

Inland marine insurance provides coverage for equipment and other property while it’s in storage or transit on land. It protects your business from losses due to damage or theft that occurs during transportation, or while you’re storing the equipment at a temporary location like a job site.

When we recommend inland marine

Any business with transportable property, such as construction equipment or goods in transit, should have inland marine.

Get technology-powered discounts on inland marine

Today, technology makes it easier than ever to manage your assets and reduce risk.

We’re pleased to offer POWERS clients access to special discounts of up to 50% on their inland marine policies.

How? It’s simple – we reward safe operators using telematics technology.

Here’s an example:

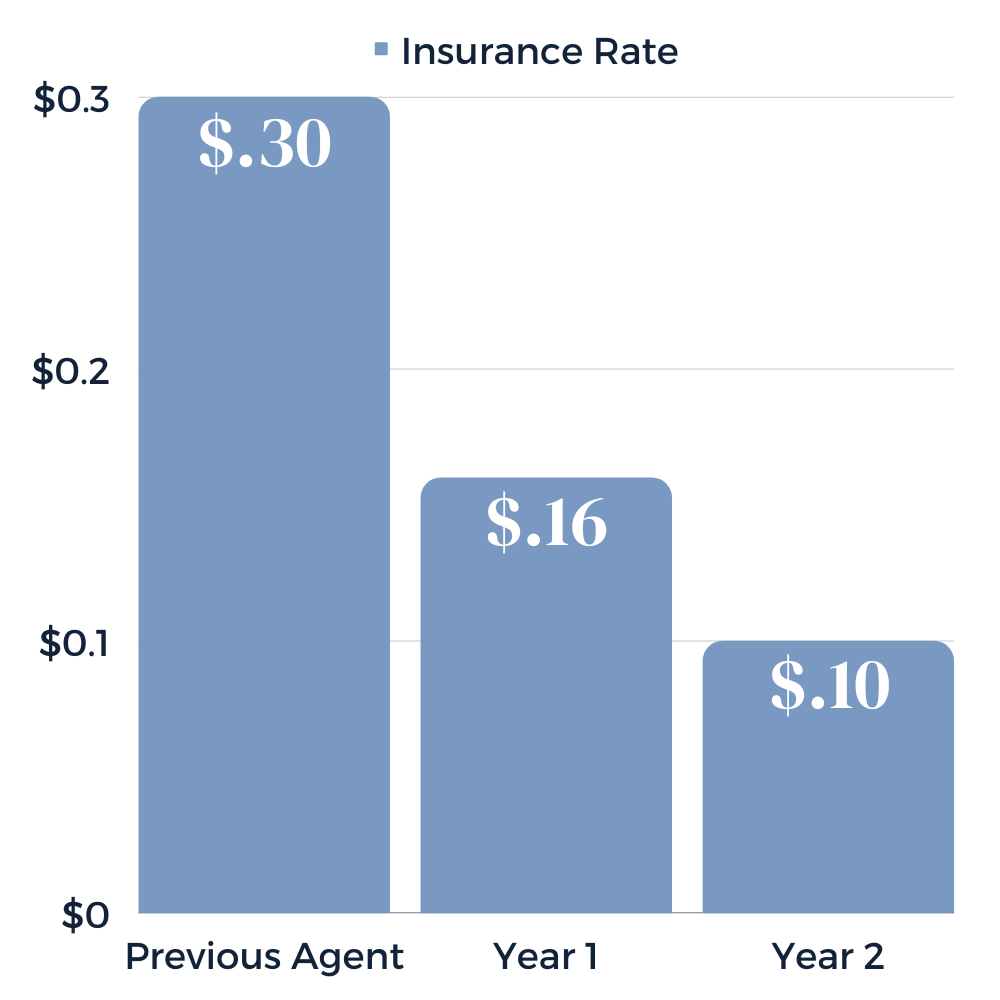

A large construction business approached us to discuss their insurance program. They decided to add telematics tech to 996 pieces of equipment, qualifying them for a proprietary discount of 47% on their inland marine policy.

Their investment in technology boosted productivity and safety – and after 12 months of no losses, we restructured their insurance program again, lowering their rate from $0.16 to $0.10. The bottom line? A 67% reduction in their equipment insurance rate over just two years.

Find out how much you can save by getting a free consultation on our calendar.

Commercial auto with HNOA endorsement

Commercial auto insurance covers vehicles used for business purposes. In most states, it’s required for commercial and personal vehicles. In case of an accident, it helps cover the cost of:

- Repairs to your vehicle

- Medical costs

- Damage to property

- Legal expenses if someone sues you

If your employees use their own vehicles for business or deliveries, their personal auto policies might not cover accidents on the job – or may not sufficiently cover your business. A hired and non-owned auto (HNOA) endorsement covers your business for liability-related claims stemming from the use of vehicles not owned by your business.

When we recommend commercial auto and HNOA

We recommend commercial auto for businesses that use vehicles for business purposes, such as deliveries. If employees are using personal vehicles for business, we also recommend the HNOA endorsement.

Builder’s risk

Builder’s risk insurance covers buildings while they’re under construction or renovation. It protects structures, materials, and equipment against damage or losses due to fire, theft, vandalism, and weather.

When we recommend builder’s risk

Any business that builds or renovates structures, like contractors or developers, should have builder’s risk insurance.

Errors & omissions (professional liability)

Errors and omissions insurance defends your business against claims that mistakes or negligence caused financial harm. It’s essential for businesses that provide professional services. It covers the costs of legal defense, settlements, and judgments.

When we recommend E&O

We recommend E&O insurance for any business that provides professional services. This includes industries like accounting and legal, as well as construction firms providing design or engineering services.

Directors & officers (D&O)

D&O insurance provides coverage for the personal liability of your company’s directors and officers. It covers claims made against them for management errors like breaches of fiduciary duty or lack of corporate governance. This policy helps protect both your company and your officers from lawsuits.

When we recommend D&O

Any business that has directors or officers can benefit from having D&O insurance to protect their personal assets.

Employment practices liability insurance

EPL insurance covers employee claims of wrongful employment practices like discrimination, harassment, or wrongful termination. It covers:

- Legal defense costs

- Settlements

- Judgments

When we recommend EPL

We often recommend EPL insurance for businesses with larger numbers of employees, but any company with employees faces the risk of employment-related claims.

Product liability

Product liability insurance covers claims that your product caused injury or property damage. It’s a common policy for businesses that manufacture or sell products. It covers costs related to a product liability claim, such as:

- Legal defense

- Settlements

- Judgments

When we recommend product liability

We recommend product liability coverage to any business that manufactures, distributes, or sells physical products.

Pollution liability

Pollution liability insurance protects your business from financial losses resulting from environmental contamination. It can cover the costs of cleanup, legal fees, and damages to third parties.

When we recommend pollution liability

We recommend pollution insurance for businesses in industries with potential environmental risks, like construction and waste management.

Cyber liability

Cyber insurance covers losses caused by a security failure or data breach. It’s beneficial for any business handling customer data. It covers a range of expenses, like:

- Credit monitoring

- Public relations

- Legal fees

- Regulatory fines

- Business interruption

- Deceptive and fraudulent instruction

When we recommend cyber liability

Nearly every business is exposed to cyber risk. We recommend cyber insurance for any business that uses technology to conduct business or store sensitive information.

Crime liability

Crime insurance covers losses caused by criminal acts like:

- Theft

- Robbery

- Fraud

- Embezzlement

These acts could be by your own employees or third parties. It covers the costs of investigations, legal defense, and judgments.

When we recommend crime insurance

We recommend crime insurance to most hospitality businesses as they’re vulnerable to crimes like theft, robbery, and fraud.

Excess liability

Excess liability coverage is for losses that exceed the limits of your other policies. It can help protect your business from the devastating financial impact of a catastrophic loss.

When we recommend excess liability

Excess liability is an extra layer of financial protection for your business. We might recommend it if you are exposed to the risk of serious claims that could quickly exceed your limits.

How much does road construction insurance cost?

Construction insurance premiums are often higher than those in other industries because of the perceived high level of risk involved. Insurance companies calculate your premiums using several factors:

- Industry and operations

- Revenue

- Payroll

- Years in business

- Claims history

- Risk management practices

Because insurance costs can vary, it’s important to work with a risk manager to find the best solution for your business. Highway and road construction companies will find the most value from partnering with an independent insurance agent that will help them proactively manage risk for long-term success.

Learn more about the benefits of integrated risk management.

Growing your road construction business with surety bonds

If you work on government contracts, you’re likely required to have surety bonds. In the construction industry, private contracts also sometimes require bonds. They mitigate risk for your client and enable you to bid on and win larger jobs.

A bond is a three-party contract between you (the principal), your client (the obligee), and the surety provider. If you fail to perform according to the contract terms, the surety will step in to fulfill your obligation.

In this event, the surety provider will expect to be made whole via the indemnity agreement, which is both a corporate and personal guarantee from you to the surety.

The main purpose of bonds is to provide assurance to taxpayers that the projects they’ve paid for will be finished, and the laborers, subcontractors, and suppliers will be paid for their work.

The most common types are:

- Bid bonds protect the obligee if a bidder wins a contract but fails to sign the contract or provide the necessary additional bonds. Bid bonds help screen out unqualified bidders, since a surety will not issue a bond to a contractor it believes can’t fulfill the contract.

- Performance bonds guarantee the completion of a project according to contract terms if the principal fails to fulfill the contract terms.

- Payment bonds ensure that subcontractors and suppliers are paid for labor and materials if the principal fails to make payments.

Bonds vs. insurance for highway and road contractors

The main difference between a bond and insurance is which party is ultimately responsible for financial losses. A surety bond is more like bank credit than an insurance policy. If the surety pays out on a claim, the principal remains liable and must repay the surety.

How contract bonds help grow your road construction operation

A bond program gives you the ability to bid on and secure government contracts. Even for a job that doesn’t require bonding, you might be required to secure a bondability letter or bid bond. These are part of the prequalification process and help the project owner weed out unqualified bidders.

Securing bonded contracts boosts your revenue and fuels your growth by:

- Allowing you to bid on larger and more complex projects

- Improving your reputation

- Helping you build the company’s financial strength and generational wealth

Need help applying for a bond or increasing your capacity to win bigger jobs? Our in-house bond experts can perform a balance sheet analysis to help you make the best bonding decisions.

Managing risk in highway and road construction: 6 common risks

Construction work involves many risks that can result in bodily injury, financial losses, and legal disputes. Here are some of the top risks and how to mitigate them.

1. Safety hazards in road construction

Job sites are hazardous. An accident can lead to a variety of negative outcomes, such as employee injuries, property damage, reputational damage, and lower productivity.

To mitigate these risks:

- Carry the proper workers’ compensation and general liability coverage

- Create documented, project-specific safety plans and procedures

- Provide regular safety training to employees

Our in-house safety education experts can help you develop both holistic and project-specific safety programs. We can also conduct training for you.

2. Damage to property and equipment during road work

An incident can damage expensive property and equipment – whether it’s yours or someone else’s. To prevent property damage:

- Ensure you’re covered with commercial property, general liability, inland marine, and builder’s risk insurance

- Monitor equipment with telematics to prevent theft and maintenance issues

- Train employees on equipment Standard Operating Procedures

3. Delays in highway and road projects

Delays in project construction can lead to additional costs, liquidated damages, and other penalties. To mitigate these risks, develop detailed project plans, provide adequate resources, and manage schedules effectively.

4. Environmental impacts from road construction work

Road construction can have environmental impacts like unintended soil erosion or the pollution of nearby water and air with hazardous material.

These harmful impacts can lead to hefty fines for your company and reputational damage. To prevent them, make sure you follow environmental regulations, take steps to minimize your impact on the environment, and consider pollution liability insurance.

5. Legal disputes in highway and road contracts

Construction projects can lead to legal disputes with clients, subcontractors, or suppliers. Insurance can cover the cost of legal fees and damages awarded in these disputes.

6. Reputation risks for road contractors

Accidents or delays can damage a company’s reputation. The best way to mitigate this risk is to prevent these incidents in the first place with consistent processes and safety policies. Insurance can help offset the costs associated with any incidents that do occur.

Choosing a risk partner that understands your road construction business

To protect the business you’ve worked hard to build, insurance alone is not enough. It’s crucial to identify the most critical threats and make strategic decisions that will allow you to grow your business without disruption.

Construction businesses face unique challenges. We’re right there with you – we work in the construction industry too. We just happen to be on the risk management side.

When you partner with POWERS, we’re more than your insurance agency. We’re a true business partner invested in your success. Our philosophy combines:

Deep Expertise

Battle Tested Processes

Cutting-edge Tools

Genuine care for clients

We put programs in place to help you execute your business plans. It’s all about empowering you to mitigate risk and grow your business. That’s the POWERS Promise.